Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2023 – Quarter 1

1Q 2023 – The Quarter Systemic Risk Reappeared

{Please be sure to read the entirety of this letter, as there are some critically important announcements regarding statement timing and changes to investor reporting cadence}

With a headline like that, one would assume the market indices would have declined in the first quarter of 2023. That would have been an incorrect assumption, as major stock and bond indices rallied. Technology stocks led the way after taking a bludgeoning last year and investors appear to be “hoping” the Fed is going to stop raising rates with the May increase of 0.25%. We have been quoted many times saying, “hope is not a good investment strategy,” and we do not believe it will be successful this time either…

As discussed last quarter, something quite unusual is happening in the world of interest rates. The Federal Reserve (“Fed”) has stated many times that they intend to remain diligent to combat inflation, including continuing to raise rates if necessary, and yet the markets are pricing in that the Fed is actually going to lower interest rates between now and the end of this calendar year. They both cannot be right and that is what makes a market, but it is very atypical for investors to show such a disregard for the Fed statements and policy mandate.

After watching the implosion of the regional banks over the last few months, it does make one wonder if the markets are pricing in a much deeper and painful recession that would force the hand of the policy makers to rescue the economy. That would beg the question as to what the stock market is paying attention to. Make no mistake, the bond market cannot be right in forecasting a horrific decline in the economy and the stock market to be right in forecasting a soft landing and that earnings are going to recover quickly. One of them is going to be very, very wrong and investors on the losing side of that equation are going to suffer some material pain.

For reasons we will detail in a moment, we remain in the camp that the Fed is going to keep rates higher for longer and that the economy is going to deteriorate more than investors are expecting. For this reason, we remain very concerned about the risk/reward in the markets and would strongly recommend investors focus on preparing for the opportunities from the dislocations that are starting. We remain a “1” on the CAZ Scale, and we strongly believe the risk/reward from these levels is not favorable. Opportunities are coming and we are building our war chest to take advantage of them. If you have not become familiar with what we are doing in the area of dislocations, please contact us and we can provide you with all of the details.

Which Fed Playbook Should Investors Use?

This is a fascinating topic for investors in 2023. In order to shed light on this answer, one must be a student of history, and not be influenced by recency bias. We all would be wise to heed the words of Winston Churchill, “Those that fail to learn from history are doomed to repeat it.” For the last ~40 years, the Fed has utilized a very simple playbook, which is to flood the system with liquidity whenever the economy starts to hit the skids. They have lowered interest rates quickly and used all the tools in their tool chest (Quantitative Easing etc.) to stabilize the economy. This has been a successful strategy for all parties, due to the primarily deflationary environment we have had over those ~40 years. We have seen this play out over and over, whenever there has been an episode the Fed has been forced to respond to. Examples of this would be the Asian currency crisis, 9/11, the bursting of the housing bubble, and of course, COVID. One can refer to this as the “Episodic Recession Fed Playbook.”

Therefore, the overwhelming majority of investors have lived most of their adult lives with a static Fed playbook. However, that is not the only playbook the Fed has used in the past. There have been several times in their 100+ year history where the Fed needed to slow down the economy and they utilized a different playbook. In times of high inflation or overly loose credit environments, the Fed has raised rates aggressively and, in some cases, drained money from the system. In those situations, the Fed was forced to use a different playbook, and one can refer to that as the “Manufactured Recession Fed Playbook.”

Simply stated, if the Fed is forcing the economy into a recession in order to win a war with inflation, there is a low probability they are going to turn around and lower rates until they are certain they have won the war. Unfortunately for investors who are not over the age of at least ~65 years old, they have never lived through a recession where the Fed utilized this playbook. The Fed has also shown us their resolve by raising rates faster than any time in history. If we use history and the Fed’s own actions as our guide, they tell us that the Fed is likely to hold rates higher for longer and may increase rates more if that is required. On May 5th, two days after the Fed raised rates another 0.25%, which the market hoped was going to be the last hike of this cycle, the April jobs report was announced. The statistics showed that the very tight labor market continues to be resilient, and more data like that is likely going to make it very difficult for the Fed to navigate the next few months without having to shock the markets with another rate increase. It looks more and more likely that we will have a tight labor market and a weakening overall economy, which is very challenging for the Fed.

Making the Fed’s job even harder is the implosion we have seen in the banking sector, with failures at Silicon Valley, Signature, First Republic, and a last-minute rescue of Credit Suisse. The speed at which these large and previously well-respected institutions failed is staggering. Much has been written about why there has been so much pressure on the banks so we will refer you to those many detailed articles and focus this letter on the fallout and repercussions for investors. Short answer… it is a problem that is likely not yet fully appreciated by the markets.

What is very clear from the data is that the economy is slowing rapidly and is likely to get worse over the next several quarters. Virtually all the leading indicators point to a material recession. We have talked extensively about the accuracy of the yield curve to predict recessions, so we will not belabor that point other than to say the yield curve is now the most inverted (182 basis points) it has been since the statistics became readily available, in 1980… Remember the statement above about how either the bond market or the stock market is very wrong?

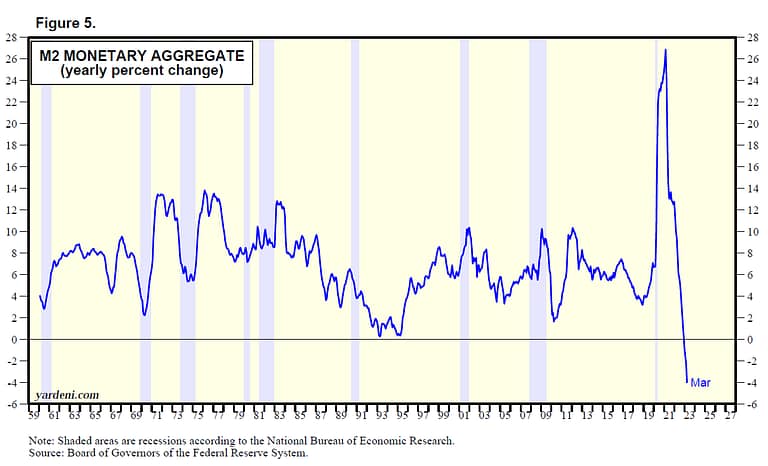

The economy is adjusting very rapidly to a different regime, which is tightening monetary conditions. Between higher interest rates and stress to the system caused by previous exuberance, the availability of credit has tightened at a nearly unprecedented rate. To put into perspective how much liquidity has left the system in the last two years, the M2 money supply year-over-year change has collapsed from an increase of ~26% in 2021 to a decline of 4% last month. That is a radical shift and this negative year over year decline marks only the fifth time that has happened since 1868, and the first time since 1930! Yes, that was in the middle of the Great Depression… Here is a visual that shows how dramatic the move has been:

This means the battle the Fed is facing is extraordinarily complex and will not likely be resolved in a way that spares investors from experiencing material pockets of dislocation. What we believe can be stated with confidence is that investors need to approach the market with the assumption we are entering a recession that is likely to be followed by a period of stagflation. That is where the economy recovers from the recession but is relatively stagnant and there is persistent above-target inflation. Those factors combine to make it very difficult for the Fed to do much to stimulate the economy, or they risk reigniting inflation. Likewise, they cannot raise rates to combat inflation without potentially tipping the economy back into a recession. Those challenges are why stagflation has proven to be the most challenging economic regime throughout history for both stocks and bonds. It is an environment most investors below the age of 65 have never lived through and will likely require a different investment approach than they have ever used before.

Where There Is Pain There Will Be Opportunity

No one likes to see financial markets stressed, as it is much more enjoyable for everyone to be making lots of money. Unfortunately, investors must be prepared to invest in all different types of markets and to identify pockets of opportunity without letting emotion get the best of us. This cycle is likely going to test even the savviest and steel-nerved allocators of capital. But there will absolutely be opportunities and one must begin to anticipate where they will be in order to maximize the profits from the dislocations.

There are some areas of dislocation that are already present in the market, and we will defer to our more detailed presentations for explanation of each of those current themes and how we are personally investing in those areas. For this letter, we feel it is important to articulate where we are beginning to see stress to help inform decisions and why we make the statements we do about the economy and the Fed.

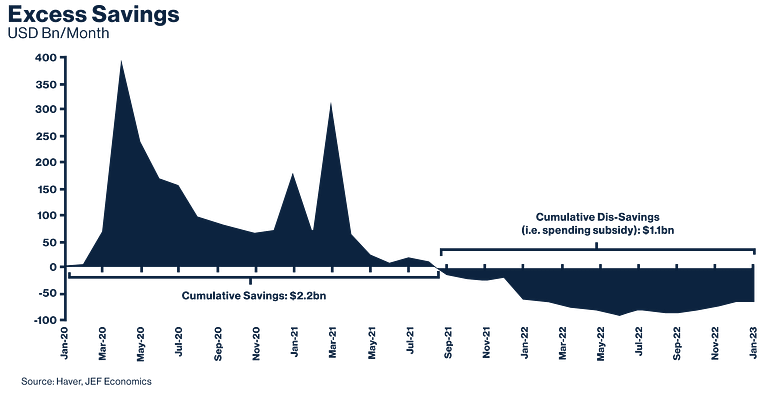

The U.S. consumer is beginning to be as stressed as they were in 2009. In some ways it does not feel that way because unemployment is so low. But the data shows us that a lot of the resiliency that may appear to exist when one goes to restaurants and to hotels may be a façade. Naturally, there is a lot of pent-up demand from the pandemic, and it also appears consumers have gotten very used to their level of consumption and will not give it up easily, even if that means increasing their debt levels. For perspective, as the chart below shows, the excess savings that occurred when consumers were being given government subsidies during the pandemic has now evaporated and has become excess spending, with more than $1.1 Trillion of consumption coming from sources other than income. This is only likely to accelerate in a recession.

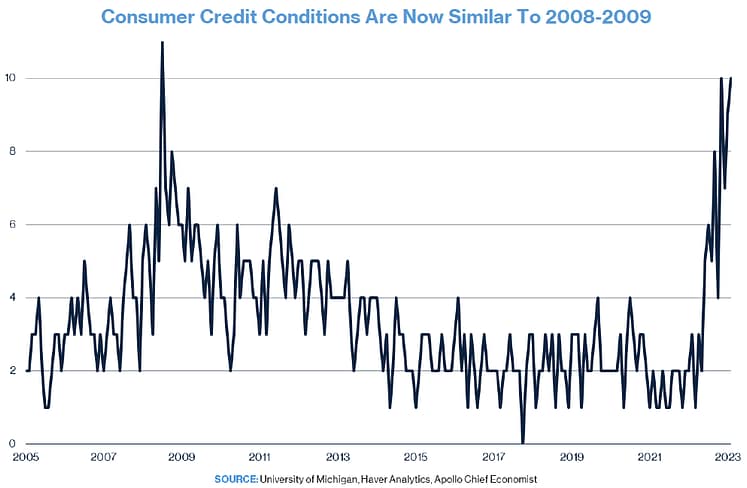

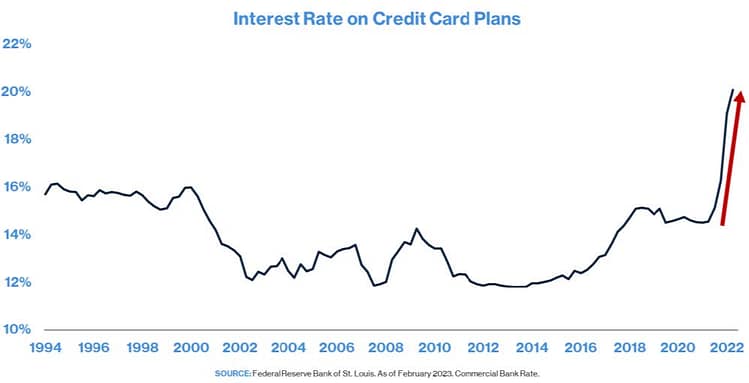

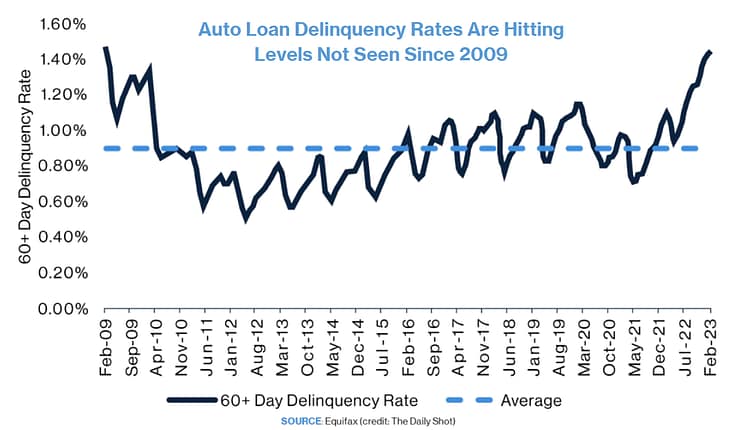

This is a slow-motion train wreck that has historically been quite painful. Below are three charts that show the tremors that are beginning to be felt through the economy. The first shows that consumer credit as a whole is now as tight as it has been since the Global Financial Crisis (“GFC”). The second chart shows how increasing interest rates are strangling the millions of consumers that have credit card debt. Yes, that really does say the average credit card now charges more than 24% interest!! The final chart shows that default rates on automobile loans are the same as the worst levels experienced during the GFC… did we mention that the current recession is just getting started?

There is additional data that is just now coming into focus, such as several consumer businesses where sales fell off a cliff in March. In some cases, year over year declines have exceeded 20%. Quite simply, there are very few businesses that can adjust fast enough to account for such a rapid decline in revenue.

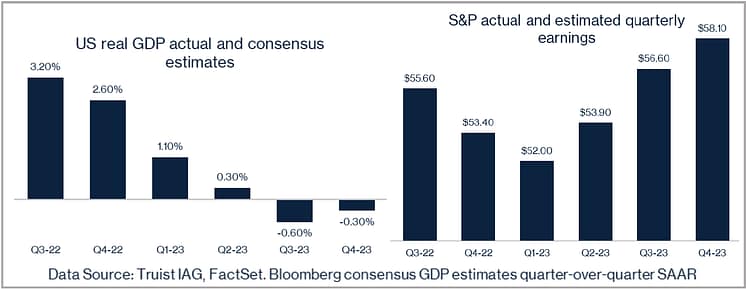

Yet, despite the expectations that the economy is going to continue to deteriorate, Wall Street analysts are optimistically forecasting a sharp recovery in earnings by year-end. Something seems very wrong with this picture:

If it sounds like a recurring theme, it is, but it is very difficult to see how both pools of analysts can be right. If the economy continues to weaken for the rest of year, it is very likely that earnings are going to weaken, and it is really hard to see how there would be a sharp rebound…

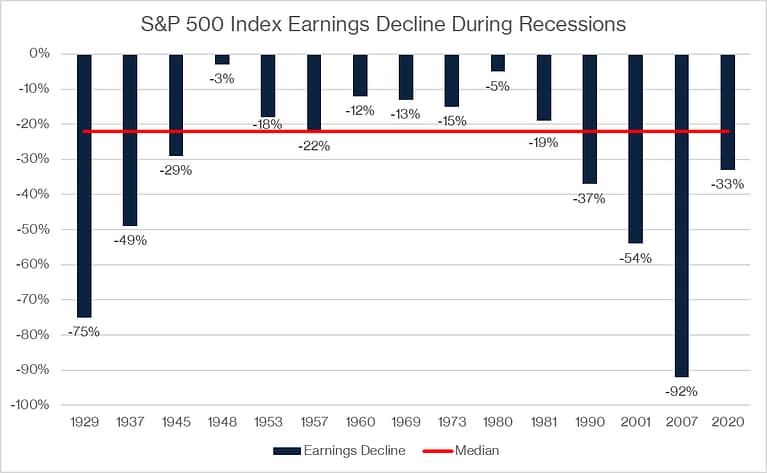

Again, it pays to learn from Winston Churchill and be a student of history. If one believes the yield curve and leading indicators which signal that the U.S. economy is going to experience a recession, we can review how earnings have performed during those periods. Every economic slowdown is different, but one thing is consistent across time, which is that earnings are challenged in those periods, particularly in a stagflation environment. Here is a chart that shows the actual earnings decline for the S&P 500 in every recession since 1929. The median decline is more than 20%.

History is not on the side of the analyst community that is estimating this cycle has already experienced the nadir of the earnings decline and that we will just go up from here. What is equally concerning is how valuations remain high, despite the pullback in 2022, particularly in light of the rally experienced so far in 2023. When one combines relatively high valuations with likely too high earnings estimates, it can be a bad combination. Let’s look at some very straightforward math:

The current 2023 earnings estimate for the S&P 500 is ~$220, and on May 6th the closing price of the index was $4,136. That means the Price/Earnings (“P/E”) multiple for the current year is 18.8. Even if one assumes there is only a mild recession, which causes current earnings estimates to be 15% too high, earnings would be ~$187. Further, if one assumes that the P/E stays the same, the S&P 500 would decline by 15% from current levels. But, if one is realistic and deduces that the pain of the recession causes the market to reprice risk and reduce the P/E multiple to just 15x, which may still be an elevated multiple for this type of interest rate environment, stocks would experience a drop of more than 30%! Anyone who believes that is not possible is not willing to accept history as a guide and may be doomed to repeat it.

That does not mean it will happen, as the economy is an ever-changing animal, but if fear and greed remain part of the human psychology, we must assume that it can happen, and invest our capital accordingly. For our personal capital, we will prepare for what is possible and respect risk. This is why we are focused on durable, cross cycle investments that should not require a strong public stock market to provide us with solid risk adjusted returns. Further, we are building our war chest to profit from what we see as the best opportunity in dislocated assets since the GFC.

The Debt Wall is Upon Us

The easy money environment that existed from 2016 – 2019 and then post-COVID, created some of the most dramatic increases in asset values ever seen. A major byproduct of those easy money policies was that risk was less respected and commercial loans were distributed by the trillions with 5 to 10-year maturities, many of which were made with very lenient terms. The interesting thing about this cycle is residential real estate lenders learned their lesson from the housing bubble and so maintained some level of discipline. Therefore, we are less concerned about the residential real estate sector than might typically be the case during a recession. As for commercial lending standards… that is a different story entirely, and the vast majority of those aggressive loans will mature in 2023 – 2027.

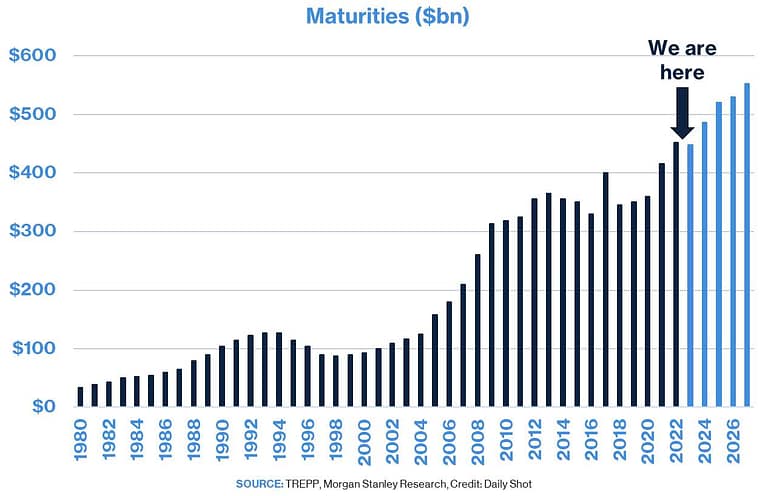

One area of immense concern is commercial real estate. The misery being experienced by those who own most office buildings is well-publicized, but not enough is being said about the looming debt wall in virtually every corner of commercial real estate. Here is a chart that illustrates the coming maturities of debt over the next five years:

One could argue that the magnitude is of little concern, as the market is much bigger than ever, but what that observation misses is the makeup of the underlying collateral that is backing those loans and the lender who originates the debt. As one would expect, most of these loans were made in a very low interest rate environment with very relaxed terms. Now rates are significantly higher, and credit is less available than it has been since 2009. Adding fuel to what is a burgeoning fire, most people are probably not aware that the largest providers of commercial real estate loans are small to medium sized banks. We have already established how much pain is being experienced by those institutions, so how much appetite will they have to provide financing to address these loans when they come due? And what interest rate will they charge?

Imagine you bought a real estate asset for $100 million in 2019 and took out a very conservative loan for $60 million and put up $40 million in equity. (Side note: Very few actually invested that much themselves, as they used preferred equity or some other instrument to increase their leverage, but let’s look at the conservative borrower…) That conservative loan likely had very friendly terms and let’s assume it carried a 4% interest rate with a 30-year amortization schedule, but the loan must be repaid in 5 years. This was very, very common and makes up a large portion of the chart above. Thus, in 2024 that loan will be due and we are likely to be in a very different environment in which that loan must be refinanced. Even if we omit the carnage that would have occurred to the value of most office buildings in a post-COVID world, and look at other areas of commercial real estate, we can definitively say that interest rates are most certainly going to be more than zero and that cap rates (the valuation metric for real estate) will absolutely be higher as a result.

Continuing with the analysis, we would be very safe to assume the asset is likely worth at least $20 million less than it was in 2019. That means there is now an $80 million value the borrower can use to refinance their loan. Even if we assume the banks will still make the loan at 60% of the current value, there is only $48 million available to borrow with which to pay off what would be a $57 million loan balance. Now the reality is the banks are unlikely to really offer a 60% loan to value in 2024, but even if they did the owner of the building would still have to come out of pocket for the $9 million shortfall. For illustration, if the banks were only willing to lend 50% loan to value, the shortfall would be $17 million. There will be some borrowers who can find a way to come up with that cash to save their investment, but many others will not, and those assets will need to be restructured or be foreclosed on. And, if the borrower did indeed utilize preferred equity or another means to increase their leverage they are likely completely wiped out. In most any scenario one can design, the equity holder will suffer material capital destruction and there will be immense opportunities for those who have dry powder available.

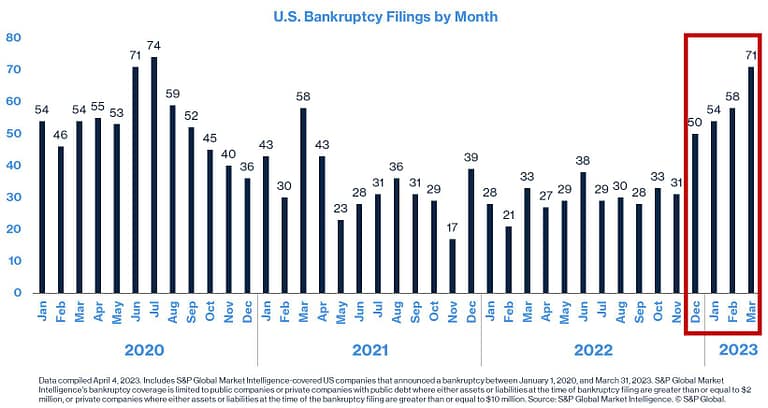

A similar story is playing out in the world of leveraged finance, and we are already seeing a rapid increase in the number of bankruptcies. Here is a chart that shows how we have seen the pain accelerating every month this year.

Like in the real estate example above, the investor who can roll up their sleeves and get involved in those messy situations will have the opportunity to be significantly rewarded. It is for these reasons, and many more, we are building our war chest to be prepared to profit from the window of opportunity we expect to exist in the 2nd half of 2023 and over the next few years. We expect these dislocations to be as attractive as anything we have seen since the GFC.

An Improved Investor Experience

We hope everyone has benefited from the multiple years we invested in the creation of the new CAZ Investor Portal (“the Portal”). If you have not spent time in the system, we would encourage you to do so as investors have been very pleased with the level of detail and transparency it provides. As the next step

in our efforts to provide you with a world-class reporting experience, we are going to accelerate the timing of which we can deliver current market values to you. This is only possible via the capabilities of the Portal and is another reason it is critical that you become well versed with that system.

Going forward, we will be delivering all performance and market value information as soon as it is available. Historically we were constrained to deliver the information once the entirety of the data was available, which meant that we were subject to the slowest common denominator. The Portal enables us to eliminate that practice and now will be updated immediately when the accounting is complete for a Fund. You will still receive a consolidated statement that shows all your information in one report, and it will be delivered in a shorter timeline than previously.

As a part of this change, we will now be able to deliver data for our drawdown-style vehicles (essentially any vehicle that owns private assets) without a one-quarter lag, as they were historically.

For full clarity, there is still no way to report data to you until it is delivered to us, of course. So, the quarterly consolidated reporting cycle will be adjusted to approximately 115 days after quarter end to reflect that reality, but we are going to install some new communication methods to get everyone the information as soon as it is available. First, the Portal will be updated for each vehicle as soon as values are received from the administrator. Second, for all liquid funds, we will begin sending email correspondence as soon as we receive the accounting for that period. For weekly liquid funds like Liquid Income, you will continue to receive weekly emails with your balance and performance information. For other funds that have liquidity, such as Barbell, Credit Opportunity, Risk Mitigation and Private Income, you will now receive a monthly email with your value and performance information. That data will also be posted to the Portal as soon as it is available, but you will receive an email to provide as much convenience as possible.

Another exciting technological development we are pleased to announce is our recent partnership with +Subscribe to enhance the investor experience. +Subscribe will provide an innovative digital subscription platform to streamline new investment documentation and provide a more efficient experience for our partners. Expect more details over the next several weeks as the program is launched.

The Portal and +Subscribe will provide faster access to the most current information on all vehicles and a simplified documentation process for new investments. We are confident you will appreciate these technological enhancements. The Team is more than happy to answer any questions you may have about the new tools.

Thank you for your partnership and we will continue to strive to deliver exceptional results. We hope that you have an outstanding summer and look forward to connecting with you very soon. All our very best!