Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2023 – Quarter 3

A Bit of a Reality Check

This quarterly letter has been a real challenge to write, as everything that happened in 3Q has really taken a back seat to the horrible hostilities that began on October 7th. To quote the 2nd quarter letter, the “Find What Matters” at this point is that there are now more geo-political risks than the markets have had to deal with in a very long time. Yes, the Russian invasion of Ukraine created some consternation, but that was quickly accepted by the markets as being regionalized and not a major driver of economic outcomes in other parts of the world. It is safe to say that every investor recognizes the potential for the conflict in the Middle East to have much farther-reaching implications. There will be more discussion later in the letter, but we wanted to address that topic before we started on the more standard commentary regarding the 3rd quarter itself.

The other reason this letter was a bit challenging to write is that we covered so much ground in the 2nd quarter letter, most of which is still very applicable today. We will not restate the exact same things, so if you have not read that letter, it is very important that you do so. Click HERE to access the 2Q letter on our website. It has some of the most in-depth analysis we have ever done on risk assets, why they do what they do, and summarizes the current conditions in a very robust fashion.

In some ways, the 3rd quarter of 2023 felt like a normal pause after a significant rally. In other ways, beyond the headlines, it felt like the world was beginning to accept some new realities. The market took a breather in 3Q and most all risk assets pulled back slightly, with most stock indices declining by 2 – 6%. Earnings were mediocre, but not horrible, the Federal Reserve did what people expected them to do, job markets continued to be tight, the consumer continues to show signs of stress, and the world is beginning to accept that interest rates are likely to remain higher for longer… All of that leads to a mediocre environment for risk assets, and that is what we saw in 3Q.

A Violent Move Higher in Interest Rates

The item that probably got people’s attention the most in the 3rd quarter was the dramatic move experienced in longer dated interest rates. The Federal Reserve directly controls the level of short-term rates, but market participants are the main drivers of the behavior of long-term rates. Supply and demand matter, and while the Federal Reserve has intervened in long-term interest rates occasionally in the past like they did during Covid, the markets generally adjust interest levels to reflect inflation expectations and fiscal behavior.

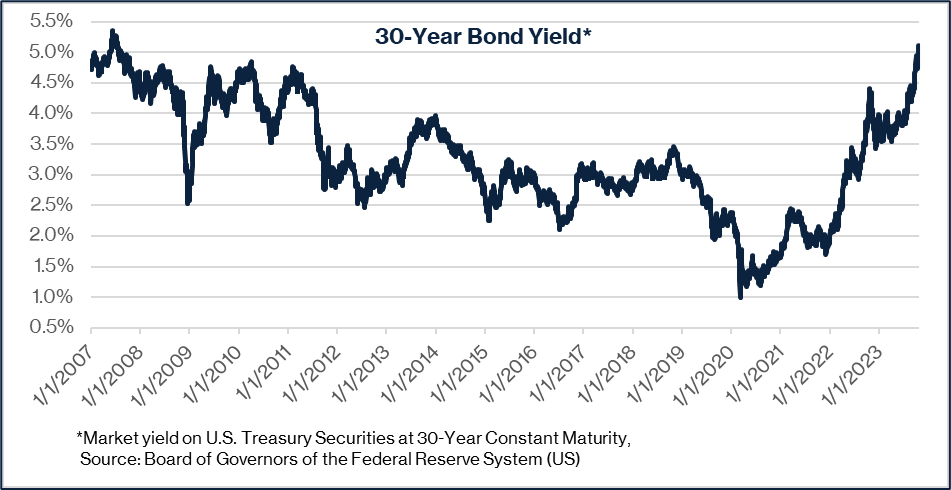

The markets reacted with a vengeance to the reality that the Federal Reserve was not likely to begin lowering short-term rates any time soon. Further, the outsized supply of new bond issuance to support the skyrocketing budget deficit overwhelmed demand. The market’s response to both items was violent and the yield on the 10-year U.S. Treasury increased from 3.84% to 4.58% and the 30-year U.S. Treasury yield spiked from 3.86% to 4.71%.

To reference our 2nd quarter letter again, that kind of a jump in yields is normally expected to have a very major impact on stock prices. The major averages did not react strongly to that move in interest rates, likely because of the enormous concentration of certain indices to a small number of stocks, but we can say that the general business community and the consumer definitely have felt the sting of that rapid increase.

30-year mortgage rates are approaching 8%, the average credit card rate for consumers has surpassed 24%, and automobile loans are quickly approaching 10%. And oh, by the way, those that have outstanding student loans must actually make payments on them again. All those various pressures are creating strain on any family that is borrowing money.

We must also consider how much inflation has impacted the purchasing power of consumers. Virtually everything a family needs has increased in price. So much so, that it now costs $734 more each month to buy the same goods and services as two years ago for households who earn the median income, according to Mark Zandi, chief economist of Moody’s Analytics.

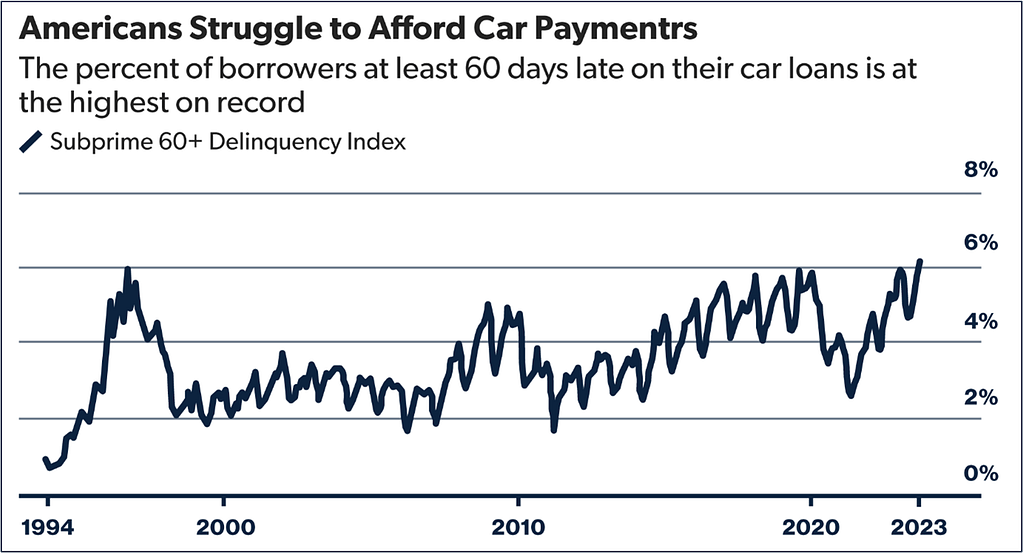

It should not be surprising then to see that delinquencies are accelerating. One of the first places that shows up is sub-prime auto loans. According to Fitch, 6.1% of all borrowers in this category are now more than 60 days past due on their payments. That is the highest level ever experienced, as in ever…

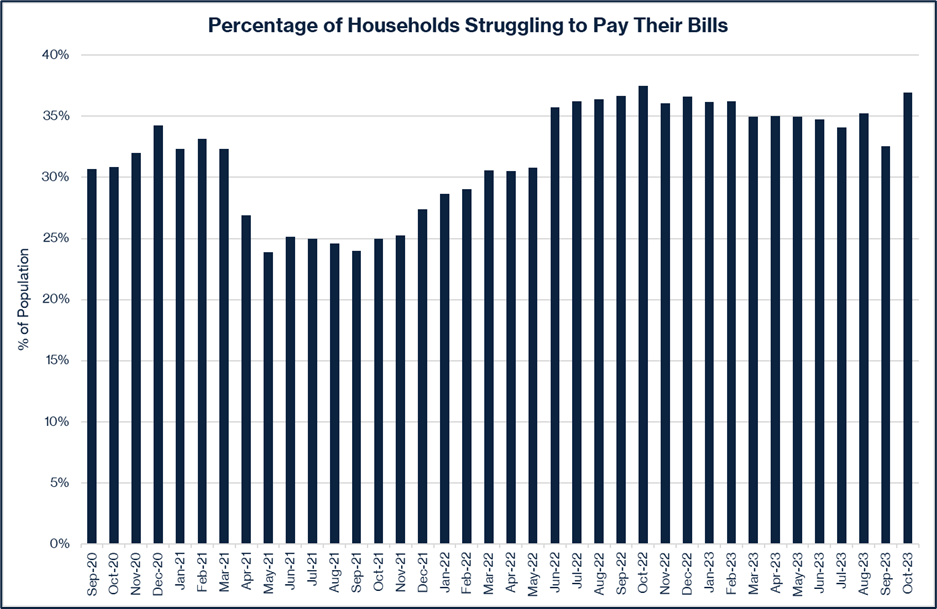

This would explain why the recent survey conducted by the Census Bureau shows the amount of stress that households are feeling. In October, more than 36% of the population said it was “Somewhat Difficult” or “Very Difficult” to pay their bills.

That is a significant spike from September, and one can easily hypothesize that it is at least partially caused by the resumption of student loan payments. For all the reasons mentioned above, consumers are feeling the pinch. The only good news is the job market remains resilient, so at least most of these families have a paycheck each month. If the employment environment starts to weaken, these consumers will find themselves between the proverbial rock and a hard place. And, of course, if the job market does not weaken, the Federal Reserve will continue to be stuck in the box we have discussed, where they have limited ability to come to the rescue out of fears that inflation will reaccelerate. This all leads to a conclusion that the stagflation we have talked about for several quarters is indeed real and likely here to stay. And, yes, that kind of economic environment has historically been a very challenging one for traditional stocks and bonds.

An Old Challenge Reignites New Risks

The conflict that erupted in the Middle East on October 7th is a reminder that the geo-political landscape is tenuous and that unpredictable things do happen, which is why it is so important to have a risk mitigation plan in place, in advance. It is impossible for anyone to predict with certainty how this war will end, but it is a lot easier to build scenarios where it escalates from its present level than it is to see how a quick and peaceful resolution is found. Let this be very clear, if Iran moves from a supporter of those attacking Israel to a direct participant, it is virtually impossible to see how this does not create a cascading impact on economic assets around the world.

Risk assets are trying to ascertain the probability of contagion and are adjusting pricing daily based on the rhetoric and the vacillating level of hostilities. What is clear at this point is that this chapter in the annals of the region’s conflict feels like it has the potential to cascade from an isolated campaign in Gaza to a more regional conflict.

That kind of an event would create a ripple effect across most asset classes, and it could also upend entirely the approach taken by the Federal Reserve and other Central Banks around the world. There is a lot more that we do not know, and cannot know, about how this will play out, but we have said many times that the thing the markets dislike the most is uncertainty. Until the region stabilizes, that is exactly what investors are going to have to deal with. And to reiterate the statement above, if Iran becomes directly engaged… all bets are off.

It is for all these reasons that we remain a “1” on the CAZ Scale, and we strongly believe that the risk/reward in traditional risk assets is not favorable. If prices decline significantly from current levels we will reassess this position, as everything becomes more attractive at a better valuation, even if the geo-political environment worsens, but it feels too early to make adjustments due to the significant changes in risk that have been created by the violence in the Middle East. We continue to believe that the current opportunities in the private markets are significantly better than what is offered in the public markets. This is especially true considering how much more attractive the opportunities are in the private markets than we have seen in quite some time.

Dislocation Opportunities are Accelerating

To build upon the previous statement, the private markets are now showing us opportunities we have not seen in a very long time. Valuations are lower, yields on private credit are higher, there are more dislocated/distressed assets, and there are fewer investors who have the courage to get involved in many situations. All of this creates significant opportunities for you.

The real estate market is following the exact road map we have talked about for a few quarters now, where the freeze in the market caused transaction volumes to plummet as the sellers did not want to accept reality and buyers knew prices did not reflect reality. Now, slowly, we are seeing sellers either willing to accept the lower prices, or just give the keys back to the lender because they have run out of options. This is likely to continue to snowball and we expect the next 2 – 4 years to provide us with immense opportunities, unlike much we have seen since the Global Financial Crisis. We are picking our spots carefully so stay tuned for more as that story unfolds.

The credit markets continue to be some of the most interesting we see, as borrowers have lost much of their bargaining position and the lenders that have capital are able to more or less set the terms they want in order to provide financing. When combined with the very significant increase in interest rates that most of these loans are based off, there have not been many times in history where it was better to be a lender in the private markets. We have spoken to the heads of many private credit firms who told us the risk/reward today is as good as they have seen in their careers, and some of these people have been in the business since the late 70’s… We are seeing immense opportunities in this area and are deploying capital in multiple unique and differentiated ways.

Private equity continues to be a bit of a dichotomy, as it is a challenging environment in which to sell assets but a very attractive time to buy assets. There are transactions occurring as there are almost always strategic reasons for acquisitions, such as the large energy purchases by Exxon and Chevron. We are now able to acquire many excellent businesses at a fraction of what they were valued at just 2 years ago, which gives us a significant margin of safety and high confidence that we will hit our return objectives.

The dislocation in energy continues to be the largest we have ever seen. There simply is not enough capital to provide for the capital expenditures needed to replenish the production required to maintain a proper supply/demand balance. This is evidenced by the gradual rise we have seen in energy prices, which began well before the conflict in the Middle East. The ability to invest in “all of the above,” from traditional sources of energy to new technologies provides us with opportunities to generate very significant returns from this sector.

We see robust and consistent opportunities in the secondary market, as the repositioning of institutional portfolios continues to be a forced behavior. The opportunity to buy from those who do not have a choice but to sell is expected to continue to generate favorable pricing for those who have the capital to deploy. Market creativity is also generating even more improved risk/reward, as many of these transactions are occurring with structural improvements that enable us to have even more downside protection.

The world of venture capital has been one of the most impacted by the repricing of risk assets, after being at the epicenter of the 2021 “bubble.” The world, generally speaking, found itself overweight in technology and the forced pause experienced by the industry has caused the pendulum to potentially swing too far. This creates opportunity for us to not only provide capital to some of the most revolutionary technology companies at a small fraction of what would have been seen in 2021, but to also acquire very attractive pools of assets from distressed or otherwise motivated sellers. Investing in innovation will always provide the opportunity for outsized gains, and doing so at much more reasonable prices creates a much-improved risk/reward proposition.

For the first time in many years, we find ourselves in a position where we have more unique and interesting opportunities than we have capital readily available. We will be introducing some new initiatives in 2024 that will accentuate our buying power and provide you with significantly advantaged ways to partner with us. At the same time, we ask you to help us grow the network by introducing us to those who are not already investing alongside you and our personal capital. As you have undoubtedly heard us say before, “The Power of the Network is the Network.” The bigger our ecosystem the more we can provide you with differentiated opportunities, so please help us expand the network.

It is startling to look up and see that we are quickly approaching the holiday season. The year has flown by, and we are already deep into planning for next year. Everyone should already have January 18th, 2024, on their calendars. That is the date for our annual Themes event, which we expect to be our biggest ever. Please plan to attend and, if you are from out of town, the hotel room blocks are open. Let us know if you have any questions and we look forward to a full day of incredibly interesting content, with additional programming on the 17th. Please check your email for more information and please be sure you register for the event as soon as you receive the official invitation. Thank you for your partnership and we look forward to seeing you very soon. All our very best!

The CAZ Investments Team