Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2024 – Quarter 3

Special Preface: This letter was completed and set for distribution before Israel’s retaliation against Iran. Please keep this in mind as you read. We have added an update at the end of this letter based on the latest information as of Sunday night, October 27, 2024.

What We Know, What We do Not Know, and What We will Know Very Soon

The timing of this quarterly letter is quite unfortunate, as the world will likely change significantly one way or another in about two weeks when the U.S. elections occur. Yes, the Presidential race matters a lot, but what would be expected to have a bigger impact on markets will be the balance of power in Congress. At this point, the control of the House and Senate are, just like the Presidential race, a virtual coin flip. There is no way to predict what the election results will be, but it is relatively easy to point to the economic implications of the possible scenarios. Gridlock, resulting from split control of Congress is pretty simple to predict. The same is true if there is control by one party of both houses of Congress but not the Presidency. What is much harder to predict are the economic policies that could be implemented if one party controls the Presidency and both houses of Congress. In that situation, the range of possible outcomes becomes much larger.

Timing is also unfortunate because tensions in the Middle East are expected to escalate in the coming weeks. Israel has clearly stated its intention to launch military operations against Iran in response to the recent artillery, drone, and rocket attacks. The situation could escalate further following the apparent direct attack on Prime Minister Benjamin Netanyahu’s personal home. As mentioned previously, if the conflict remains limited to Israel and Iranian proxies, it is likely to stay contained. However, if direct confrontations between Israel and Iran increase, the stability of the entire region could be threatened.

Another reason the timing of this letter is a challenge is that the Federal Reserve will meet in early November and their actions will loom large for financial markets. Last quarter, we discussed the difficulties consumers are encountering, and most of those issues have either persisted or worsened. Please revisit that letter for more details. We noted there that, for the first time in many years, investors seem to believe that “The Fed Put” is back, implying that everything will be fine, and valuations are irrelevant if the Fed is easing. Well, the Fed did indeed enhance those feelings of comfort, when they announced a 50 basis point “super cut” on September 18th. Since that time, we have learned from the minutes of that meeting that there was significant debate around whether the data supported the 50 basis point cut, or if it was more prudent to only lower rates by 25 basis points, with one of the Governors voting against the decision, which broke a long stretch of unanimity from the board.

The economic data since that meeting has not supported aggressive easing and now the big question will be whether they do another 25 basis points in November or if they pause to see more data. With the wildcard of the election happening at nearly the same time, it is really hard to predict what they will do. We can say with confidence that we believe the Fed made a mistake by doing the super cut. This is what we wrote last quarter:

There is a growing consensus that the Fed will cut aggressively at the September meeting and that will start the next easing cycle. Some forecasters were calling for an emergency cut in August and/or have predicted a “super cut” of 50 basis points at the next meeting. It is quite possible that the Fed will deliver a cut in September, IF the data we receive between now and then supports it, but we would be shocked if they did more than 25 basis points. Our view is that the Fed still realizes they are in a box and that the inflation dragon must be definitively slain before they can begin to feed the animal spirits once again.

We maintain our stance, with recent remarks from numerous board members underscoring our assertion that there remains significant concern that the inflation dragon may still be very much alive.

Markets can be expected to respond violently based on the three major factors outlined above. We apologize for leaving you in suspense, but the letter must be issued alongside statements. Should it be necessary, we may release a special publication after the election, and rest assured, you will receive it if we do.

Despite the potential drama discussed in the first section of the letter, we do not invest our personal capital based on expectations around the short-term impact. We will definitely adjust our focus as needed based on expectations for policy and interest rates, but with a longer-term view as to how it impacts our major themes and the investments we make to profit from those trends.

A Picture of Valuations that Should Grab Attention

Regardless of what happens in the world, one thing will hold true, valuations matter and those who ignore them do so at their own peril.

One of the fortunate things about being able to invest in either the public or private markets is we can allocate capital wherever we believe it is most likely to be successful. More often than not, we gravitate where the valuations are more attractive relative to the liquidity of the assets. We find ourselves at an interesting place in the history of markets, where private market assets continue to provide much better valuation profiles relative to their public market peers. Private market assets are currently valued at two to three times the discount at which they normally trade.

We all know the world is changing and most know that the S&P 500 index now is dominated by a few massive technology companies, with the Magnificent 7 representing more than 30% of the index. What most do not fully realize is how expensive the index is relative to history. Before talking about history, one must be intellectually honest and acknowledge that history does not always repeat itself, but it does rhyme. The broad-based index does still represent the economy as a whole despite its concentration, and ultimately the world will need growth of earnings in order to create jobs and demand for goods and services. Thus, we can all agree that markets will still go up and down and that performance will be overwhelmingly impacted by the valuations for assets at the beginning of any time frame we want to consider.

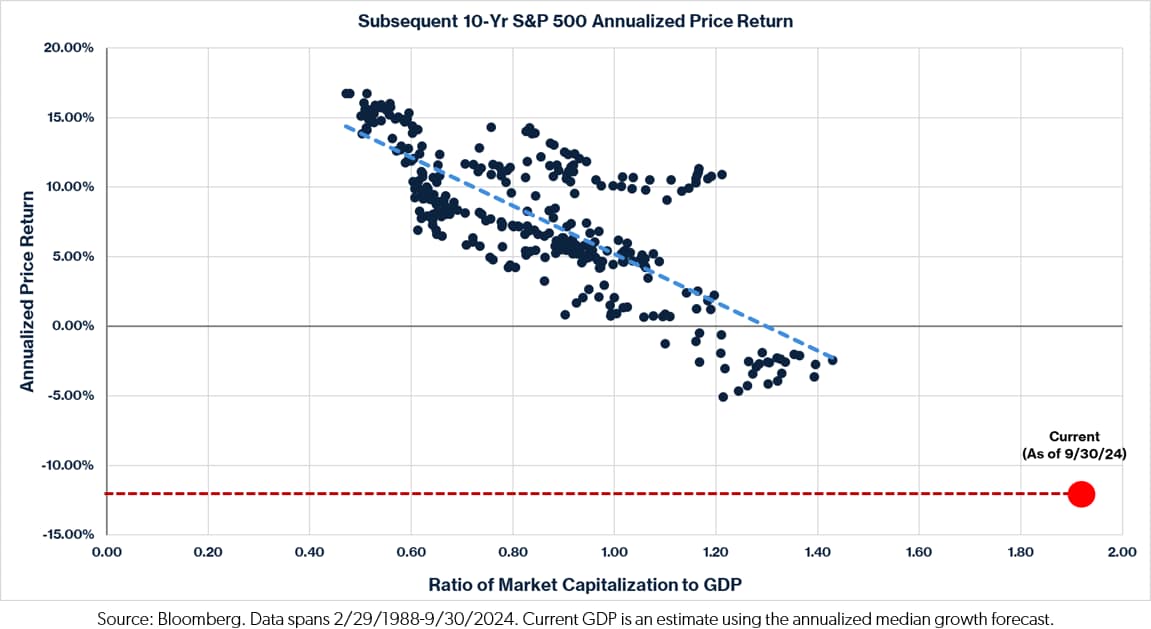

One of the tools that we use personally when making allocation decisions is the Buffett Indicator, made famous by the most famous investor, Warren Buffett. Not only has it been shockingly accurate, but it is also amazingly simple, in that it eliminates the noise and arguments about stock index constituent size, accuracy of analyst earnings estimates etc. It just looks at the ratio of market capitalization to Gross Domestic Product (“GDP”). Interpretation is also very straightforward in that you track the starting level of the indicator on a given date and how the S&P 500 has performed over the subsequent 10 years and place a point on the chart shown below. You then do that for each 10-year period and the trend becomes exceedingly easy to spot. When the market capitalization is low compared to GDP, stock market returns are good for the next 10 years. When that is not true, stock market returns are not as good. And, at extreme measures, there can be outsized gains and periods of very disappointing returns, even full decades with negative compounded performance.

With that explanation how to interpret the chart, let’s look at the current indicator level:

History is clearly not on the side of the public markets. Now, one can make a bevy of arguments about why “it is different this time” and some of those hypotheses may have legitimacy, but if we look at any other number of metrics, whether it be Forward P/E multiples, Price to Sales, Price to Book, Price to Free Cash Flow, the picture is going to be quite similar. In most cases, the projected 3, 5, 10 year returns for the S&P 500 are projected to be low single digits at the best, or negative returns at the worst.

These reasons, among others, explain why we remain a “1” on the CAZ Scale. We firmly believe that the risk/reward profile of traditional risk assets is not very favorable. While there are intriguing dislocations and some good values within the public markets, we still find remarkably more appealing opportunities in less-correlated assets.

We reiterate that the poor risk/reward posed by expensive valuations does not mean that someone should sell everything they have in the public markets. But what it does mean is that if you have other alternatives, they should be considered. In our situation, we are blessed to be able to invest our personal capital anywhere, in anything, at any time. Right now, we simply see massively more attractive opportunities for consistent and predictable returns in the private markets.

Themes We are Focused On

We are very thematic investors, and we rely on those core themes to direct our efforts, evaluate new opportunities and determine where we want to allocate our personal capital. No matter how many different things we look at, which has already exceeded 1,000 this year, we will never waiver on our demand for excellent risk adjusted returns.

Each of our core themes continues to provide us with solid new opportunities in which to deploy capital, as we are known as leaders in each of the areas which enables us to triangulate relationships to access exceptional potential investments. The flow is steadily increasing in several areas, such as the Energy Evolution, Disruptive Technology, Secondaries, the Changing Needs for Military Readiness, and the Growth of Private Assets. But nowhere has there been a more dramatic change in the opportunity set than in Changes in Consumer Behavior (Cord Cutting), as a result of the NFL beginning the process to allow a few select Private Equity firms to invest in NFL franchises. We are actively engaged in those conversations and if you are not aware of what we are doing in that area, please contact our Team.

We look forward to a very exciting few months as we sprint through the 2024 finish line. Invitations are beginning to be disseminated for our annual Themes event in Houston on January 16th, 2025, with additional activities planned for the afternoon and evening of January 15th. We expect to be space constrained again this year, so please let us know one way or another as soon as you receive your invitation and start booking your travel as needed. We appreciate your partnership and look forward to seeing you very soon!

The CAZ Investments Team

Special Update: On Saturday, October 26, 2024, Israel conducted pre-dawn airstrikes on military targets in Iran. This action was in retaliation for the recent barrage of ballistic missiles Iran fired at Israel earlier this month.

As of Sunday night, markets around the world are taking the limited scope of the attack, which did not include oil related targets, as a neutral to positive outcome. The restraint that Israel showed appears to have provided comfort to the markets that the Iranian government MAY not retaliate, against the retaliation.

We will keep everyone posted on this situation, as well as the other critically important news items that are expected over the next few weeks.

If you do not already follow us on Linked In, we would encourage you to do so by clicking HERE. We will post special updates there as needed. All our very best!