Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2025 – Quarter 3

The third quarter featured significant geopolitical activity, with material progress made regarding tariffs and the cessation of hostilities in the Middle East. The economy continues to move forward at a healthy clip and inflation appears to be moderating, but the consumer continues to show signs of strain. This combination enabled the U.S. Federal Reserve to shift its policy to be less restrictive and towards accommodative. In a nutshell, it feels like we have taken several steps forward this year but we still have some major hurdles to overcome. That is normal, and what makes markets, but it is important to occasionally step away from the noise and “Focus on the Forest, not the Trees.” It is in that spirit that this communication was written. There are many major philosophical discussions facing investors and our society, and we will tackle two of them in this letter.

Update in Valuations

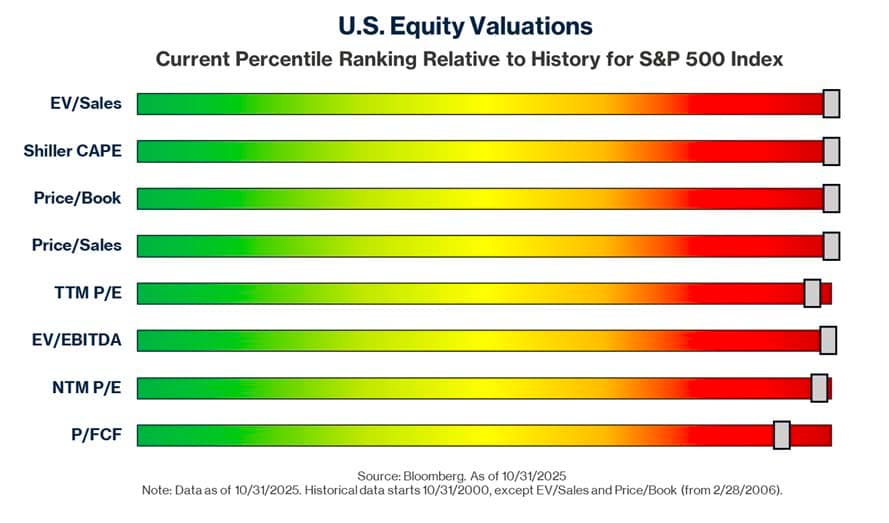

Before we jump into some very interesting discussions around the impact of AI, we need to level set on valuations. Yes, price does still matter, and we will make that case in a compelling way below. As stated last quarter, we have learned that a picture will say a thousand words, and the easier it is for investors to understand what we are trying to communicate, the better. We felt the best place to start would be best to update the chart from last quarter. As a reminder, “red bad, green good!”

The beauty of this chart is that it avoids any argument as to whether the S&P 500 is cheap or expensive, across virtually every major valuation metric that one could want to use. We find ourselves in extreme levels of red… remember, red bad…

Aside from public market valuations, we like a lot of what is happening in the world today, and it is a positive that the U.S. Federal Reserve has begun to reduce short-term interest rates. We expect that trend to continue if we see the slowdown in the economy accelerate. The consumer is under significant pressure and we do not see any major catalyst to change that dynamic, other than lower interest rates.

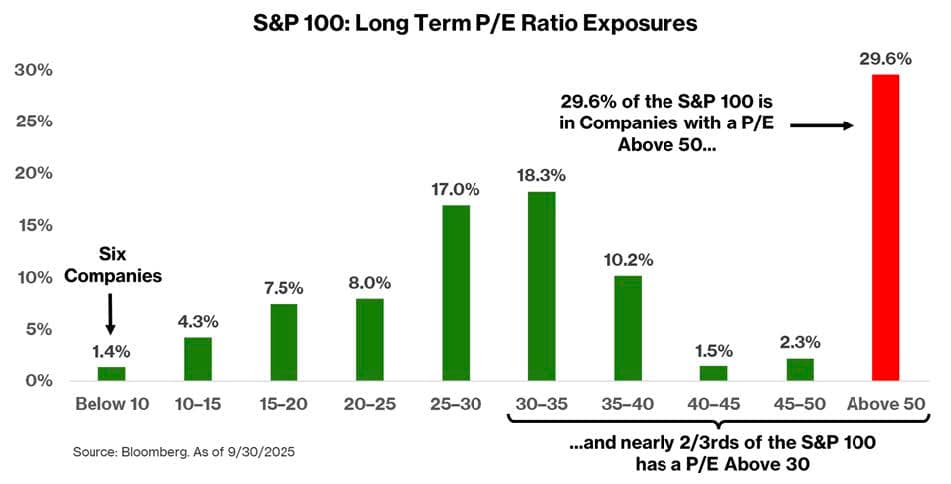

The thing that we are consistently surprised by is how little fear we see among professional investors related to the extreme concentration of the stock market. As we have stated before, more and more of S&P 500 index is now represented by very few companies. For an update, the largest 10 companies of the S&P 500 now represent more than 38% of the entire market capitalization and one company, Nvidia, makes up almost 10% by itself! Stay tuned for that discussion….

The other thing that is disconcerting is that the concentration is also accompanied by very high valuations, by any historical measure one wants to use, for the components that make up that concentration. For those that do not follow it, the S&P 100 is the index that tracks the largest and most liquid 100 members of the S&P 500. It is commonly referred to as the “OEX” and it is one of the most monitored, traded, and hedged indices. Let’s look at the Price to Earnings ratio for the members of the OEX .

Yes, you are reading that chart correctly, more than 29% of the value in the OEX is trading in excess of 50x earnings. Even more shocking is that 62% of the S&P 100 is trading at greater than 30x earnings, with just 6 of the 100 companies trading at less than 10x!

It should not surprise you to read that we remain very concerned about the valuations in the public stock market, in addition to credit spreads in the corporate bond markets. Therefore we are a “1” on the CAZ Scale. That said, when it comes to private assets, we are as busy as we have ever been and see tremendous opportunities to deploy capital with attractive expected rates of return.

The Past Does Not Always Repeat, but it Frequently Rhymes: Lessons Learned from Cisco

With the table set, let’s pivot to one of the philosophical discussions. As can clearly be seen from the charts above, markets in general are very, very expensive. A constant refrain we hear is “it is different this time,” which makes our skin crawl and is terrifying. Of course, it can be different this time, and things are rarely exactly the same, but the fundamentals of investing do not change. Price and valuation still and always will, matter. Let’s look at a case study of the poster child of today and compare it to a poster child from history.

In today’s market, few companies have captured investor attention like Nvidia. Its recent ascent to a $5 trillion market capitalization is not just a milestone — it reflects the market’s belief that Nvidia will define the future of artificial intelligence. But as we have said for decades: greatness in a business does not guarantee greatness in an investment. Price matters. And sometimes, it matters more than anything else.

This is not a critique of Nvidia’s business in any way. They have built an amazing company. It is a valuation exercise — one that echoes a lesson learned during the dot-com era.

In March 2000, Cisco Systems peaked at approximately $82 per share, with a market cap of roughly $555 billion. It was the dominant player in internet infrastructure, profitable, and essential. Yet, 25 years later, Cisco trades around $73 per share, still below its dot-com peak. The company remained strategically relevant and operationally sound and has increased its annual revenue by more than $30 billion, but the valuation in 2000 priced the company based on perfection. And perfection is rarely delivered.

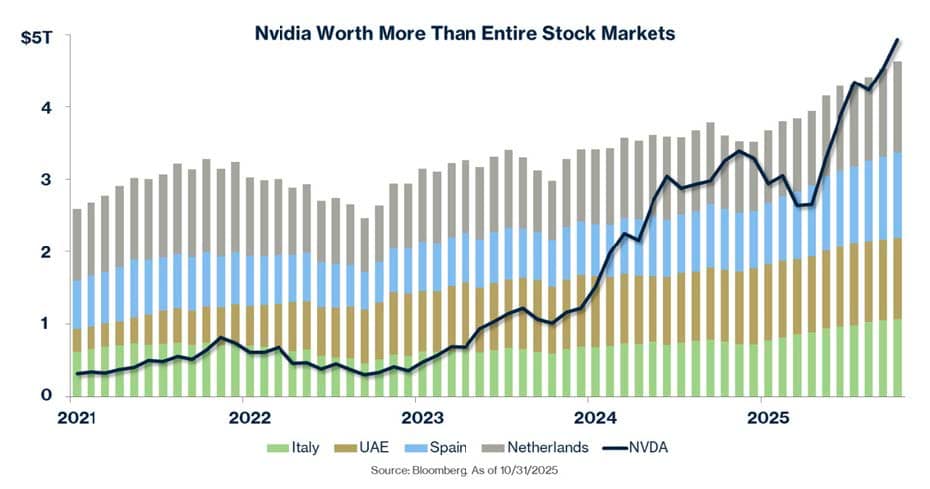

Now consider Nvidia. At $5 trillion, it represents nearly 10% of the entire S&P 500, 15% of the OEX, and nearly 20% of the Nasdaq 100, a level of concentration never seen before. Nvidia is now larger than six of the eleven S&P sectors, including very large engines of our economy such as Industrials and Consumer Staples. In fact, Nvidia is now worth more than 3x the entire Energy sector of the S&P 500 — which produces the lifeblood that the AI economy and Nvidia must have to operate…energy.

If those statistics do not astound, how about this, Nvidia stock is now worth more than the entire stock markets of Italy, UAE, Spain, and the Netherlands…combined!

To be very clear, the numbers driving this enthusiasm are staggering. AI capital expenditure from the four hyperscalers — Amazon, Meta, Microsoft, and Google — is expected to reach $440 billion next year, up 34%. Nvidia’s projected revenue for the coming fiscal year is $285 billion, up from just $11 billion in FY2020. But here is the problem: markets are now treating these extraordinary figures as the new normal, extrapolating them indefinitely.

This is exactly what happened to Cisco. The company did not stumble operationally. It did not lose relevance. It simply could not grow fast enough to justify the price investors paid.

Let’s run the math.

If an investor wants a 15% annual return from Nvidia over the next decade, the company will need to reach a market cap of $20.25 trillion. That implies annual net income of $1.35 trillion at a 15x terminal multiple to earnings.

To put that in perspective, Apple earned ~$100 billion last year. Nvidia would need to generate the equivalent of 13 Apples of profit in a single year. There is no precedent for this in financial history.

If the point was not fully made, please consider that Nvidia is valued higher than the annual economic output of nearly every country on Earth — only the United States and China have GDP larger than Nvidia’s valuation.

This is not a prediction of failure. Nvidia may very well continue to lead the AI revolution. But the valuation assumes decades of flawless execution, sustained margins, and profit generation at a scale that may exceed the plausible earnings power of the global economy.

The risk is not that Nvidia will falter. The risk is that investors are paying a price that assumes outcomes beyond what any company, no matter how great, has ever achieved.

At CAZ, we remain committed to investing in exceptional businesses. But we are equally committed to valuation discipline. That discipline has served us well for 25 years, and it remains as critical today as ever.

The Hollowing Out of the American Workforce

Now everyone should grab a beverage and join us for some very deep thinking… Over the last 12 months, a very clear pattern has emerged across U.S. corporations, particularly inside the largest employers of white-collar talent. The headlines talk about layoffs, but the underlying driver is more specific than broad economic slowdown or softness in demand.

We are seeing an AI-driven restructuring of the American workforce.

This is not theoretical anymore. It is now observable, measurable, and heavily reported. And the most important observation: this hollowing out is not happening at the bottom or the very top. It is concentrated in the middle.

Across multiple industries such as ecommerce, logistics, enterprise technology, software, manufacturing and customer-facing digital businesses, the same trend pattern is appearing repeatedly:

- Entry-level and frontline labor is not being replaced en masse by AI.

- Senior leadership is not being replaced by AI.

- The middle is being structurally eliminated.

This is happening because AI tools, particularly generative AI, now allow individual contributors to do the work that previously required two to four layers of human coordination, management, and processing roles in between.

In effect, AI allows companies to widen spans of control and compress organizational layers. The result is the removal of middle tiers that historically provided coordination, translation, documentation, prep work, content creation, etc. Here are some recent examples:

- Amazon cut approximately 14,000 corporate roles in 2025—roughly 4% of its white-collar workforce. These were not warehouse jobs. These were mid-tier knowledge roles, eliminated as the company accelerated AI investment and removed layers of internal bureaucracy. Multiple outlets tied the cuts directly to AI-driven efficiency efforts.

- UPS announced what is likely the largest restructuring in its 100+ year history, cutting between 34,000 and 48,000 jobs—far exceeding its initial target of 20,000. These were not delivery drivers. These were support functions, corporate structure, and middle layers impacted by automation, facility consolidation, and AI-powered logistics optimization.

- Microsoft eliminated ~9,000 jobs (~4% of its workforce), citing streamlining and heavy AI capex. Reporting emphasized the simplification of layers and a shift toward technical roles. Internal sources confirmed a deliberate trimming of middle managers and non-coders to boost span of control and prioritize engineering talent.

- Intel announced plans to cut more than 20% of its workforce, highlighting a drive to slash a “bloated… middle management layer” while reshaping its AI strategy. The company is not just investing in AI—it is reorganizing around it.

- Google eliminated a middle-management layer in its U.S. ad sales division (GCS), citing efficiency and the need to compete in AI-driven advertising. Broader reporting throughout 2025 has documented similar flattening across Google’s business units.

In all these cases, workforce reductions were paired with increases in AI infrastructure investment, AI engineering hiring, and platform tooling spend. The layoffs and the AI capex are two sides of the same strategy.

One of the most harrowing recent quotes was from Ford’s CEO Jim Farley, “Artificial intelligence is going to replace literally half of all white-collar workers in the U.S.”

This is not only a headline-driven phenomenon. We also see companies demonstrating where AI displaces middle-tier output:

- Duolingo replaced hundreds of content contractor functions after shifting to “AI-First” lesson generation. What once required teams of curriculum designers and editors is now being handled by generative models.

- Klarna publicly reported that its AI assistant was performing the work equivalent to ~700 customer service reps. These are not low-skill roles; they previously required somewhat advanced human coordination and judgment.

The structural impact is becoming clearer, and this movement is sometimes called the Great Flattening, a trend where companies are paring back layers of management and increasing spans of control. The message is consistent: the middle is being squeezed.

This is not just about replacing people; it is about rethinking how organizations function. The traditional pyramid is being compressed into a flatter, more technical, more automated structure.

Why This Matters Going Forward

This trend is important for investors for four reasons:

- Corporate margins may structurally expand as middle layers shrink. This is not cyclical cost cutting—it is structural OPEX replacement by computing power.

- The earnings leverage of AI is just beginning. These workforce restructurings are the early stage signals of companies rewriting operating models, not simply deploying AI as a bolt-on productivity tool.

- The labor market narrative is backward looking. Analysts have been focusing on AI replacing low-cost, low-skill work. The data suggests the opposite—AI replaces middle complexity coordination work first because it is structured and repeatable and has fewer regulatory and physical constraints.

- This will create a severe bifurcation of white-collar earnings power inside the U.S. economy in the decade ahead. Executives with strategic direction and highly technical implementers at the bottom will remain. The space in the middle could become dramatically thinner.

This is still early. Most companies are only in phase one. What we are watching right now is the beginning of the first major structural labor rewrite inside corporate America since the offshoring wave of the early 2000s. And this wave will be bigger.

Equity owners should benefit, as long as they do not overpay for the expected improvements. Middle tier workers, historically considered “safe” white collar earners, likely will be materially impacted.

As capital allocators, it is important to recognize that this is not a temporary adjustment. It is a secular shift. At this point AI is not killing jobs evenly. It is hollowing out the middle.

It is for these reasons, and more, that our Team remains laser focused on themes that should be insulated, and potentially benefit, from these trends. We want to own great assets, purchased at reasonable prices, that possess strong moats and meet irrefutable demands. That combination should lead to persistent returns with favorable risk/reward. It is in that way that we are investing our personal capital and we will keep you apprised of what we are finding across the landscape of opportunities that we evaluate each year.

As a reminder, our Themes for 2026 event will be held on January 27th and 28th. If you have not registered, please do so as soon as possible as we are nearly on a waiting list. Because of the profile of our speakers, and the fact that this will be the 10th anniversary of Themes and the 25th anniversary of CAZ, we expect to exceed capacity. Have an outstanding holiday season and we look forward to seeing you very soon.