Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2024 – Quarter 1

While drafting this letter, which has been quite challenging, there was an overwhelming feeling of Déjà vu. Regardless of which direction the letter wanted to go, it just seemed to scream “read the 4Q letter.” While we certainly will not just reprint that letter, which you can access by clicking HERE, it is incredibly important for you to go back and review that 39-page tome as it had an enormous number of charts and statistics that apply every bit as much today as they did a few months ago.

The reality is that many of the same core themes apply, and we must be fully aware of their potential impact for investment assets of all types. It is unusual for themes to sync up the way they do today, but there are six “Cs” that we believe encapsulate the state of the world. This may help everyone remember how we see the landscape today and the things that investors should be focused on. The six Cs are:

- Cuts in interest rates are not happening like investors were hoping for.

- Consumers are under increasing pressure.

- Commercial real estate is awful.

- Concentration of the public stock market is at 40+-year highs.

- Cash yields are higher than earnings yields which is usually a recipe for poor stock market returns.

- Conflicts in the Middle East and Asia are the wild card.

With that backdrop, we will highlight the key takeaways for each of the six Cs.

Cuts in interest rates are not happening like investors were hoping for:

The main point made at our Themes for 2024 presentation in January was that the “Fed is in a Box,” and that investors were going to be sorely disappointed if they thought the Fed was going to begin aggressively cutting rates. That has become an irrefutable truth, as no cuts have occurred yet and it looks like it will be several months before any happen… IF any happen before the end of the year.

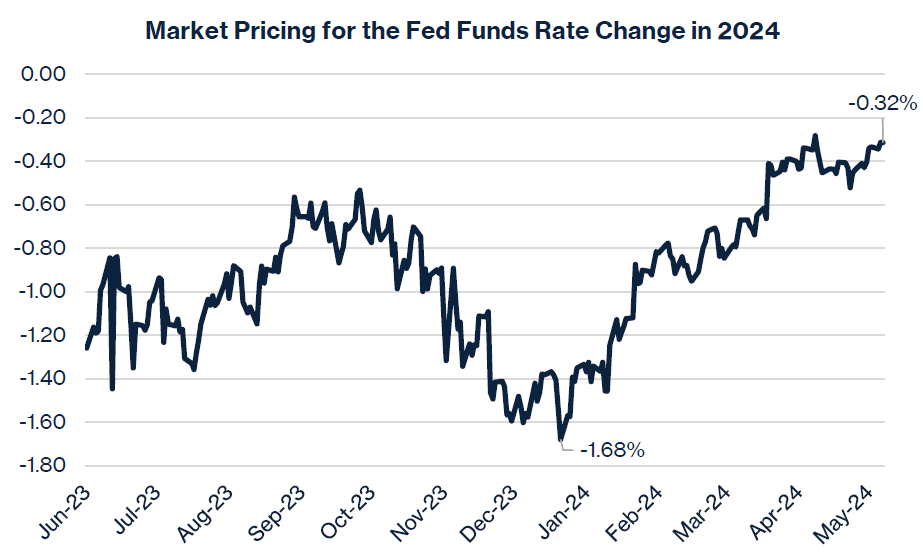

To illustrate how the market has been forced to recalibrate, a picture will save a thousand words. The chart below shows how investors were forecasting more than 1.60% worth of cuts in calendar 2024, and how those expectations have deteriorated to approximately 0.30% worth of cuts this year:

Those expectations can move quickly based on the latest flurry of economic data. But clearly, the market has reluctantly accepted the reality that the Fed is indeed in a box and will be forced to be very data dependent to avoid the catastrophe of the early 80s. To illustrate this most powerful point, on May 28th, one of the Fed governors indicated that he believed they needed to see “many months” of improving inflation data before they could act, and they might have to increase rates even more if the situation did not improve.

We remain in the “stagflation” camp, where we experience stubbornly high inflation and yet a stagnant economy, with a consumer who is beginning to feel pressures they have not felt in more than a decade.

Consumers are under increasing pressure:

This recurring theme is only accelerating as we progress through 2024. Here are a few updated data points:

- The 90+-day serious delinquency rates for auto-loans have increased in the last 18 months from 1.6% to 2.8%, the highest level since 2009.

- The 90+-day serious delinquency rates for credit cards have increased in the last 18 months from 3% to ~7%, the highest level since 2009.

- Non-mortgage interest payments have skyrocketed in the last three years from less than $200 billion to more than $600 billion and now, for the first time in recorded history, are larger than mortgage interest payments.

- 36% of households are finding it difficult or somewhat difficult to pay their bills, according to the Census Bureau’s Household Pulse Survey.

- Credit card debt has reached new all-time highs, with the average balance per borrower now exceeding $6,200, according to Experian, with the average interest rate now exceeding 24%!

The good news is that the job market remains resilient, which leads to the sticky inflation mentioned earlier, and these two disparate factors strongly support the stagflation thesis.

Commercial real estate is awful:

There are so many statistics to quote on this topic it would just take too much time to read them all, so here are a couple of “find what matters” newsworthy data points:

- Office vacancy rates are the highest they have ever been, estimated at 20%.

- The Trepp Special Servicing Rate leaped by 80 basis points last month to reach 8.11%. This means that more than 8+% of all commercial real estate is currently in distress, with highlights/lowlights in certain segments that may not fully be appreciated by investors:

- More than 1 out of 10 office properties are in distress.

- The pain in multi-family is accelerating, with 1 out of 20 properties now in distress.

The ripple effects throughout the economy are material and will not be fully known until this cycle hits bottom. What is clear is that this dislocation will influence credit availability generally and specifically impact the health of the regional banks, as they are the holders of a lion’s share of the debt on commercial properties.

Concentration of the public stock market is at 40+ year highs:

This particular statistic seems to become more astounding every quarter. The reasons for the concentration are well documented, with the “haves” in technology overwhelming the performance of the “have-nots” in the rest of the economy. The risks that it creates for index performance are clear, but what people may not fully appreciate are some of the underlying discrepancies that do not get as much attention:

- The concentration of the top five names in the S&P 500 are now the largest they have been since the 1970s, at more than 25%, with the “Magnificent Seven” representing more than 32%.

- More than 40% of companies that make up the Russell 2000 are LOSING money, and that number is increasing, not decreasing as one might expect in a growing economy.

- Over the last two years, in an inflationary environment with significant GDP growth, if the Nasdaq 100 companies were removed from the S&P 500, the earnings for the index would have actually DECLINED.

The disparity between the “real economy” and the “digital economy” has never been greater. That is logical on the one hand, as we are becoming more and more dependent on technology, but we cannot forget that the vast majority of companies and jobs around the world need to elevate in order for us to experience sustainable economic growth.

Cash yields are higher than earnings yields which is usually a recipe for poor stock market returns:

We wrote a very significant explanation on Equity Risk Premium in our 2Q 2023 letter, which you may access on our website by clicking HERE. Please read that letter, or reread it, in order to fully appreciate the statistics to follow:

- As of May 24th, the S&P 500 earnings yield was 3.63%.

- As of May 28th, the U.S. 10-year Treasury yield was 4.55%.

- The corresponding negative equity risk premium, which is an oxymoron, of -0.92% is a level that has not been seen in decades.

Simply stated, history has shown us that it is overwhelmingly unlikely that investors will experience acceptable equity returns from such a starting point.

Conflicts in the Middle East and Asia are the wild card:

The violence in the Middle East has been horrific and the risk of escalation in the region remains one of the greatest risks to the global economy. The potential for disruption of energy supplies to the world cannot be underestimated.

The Taiwan situation seems to calm down for a few months and then flare up again, to remind us of the existential threat that hostilities in the region could create. Make no mistake, a direct military action by China into Taiwan would have catastrophic implications to worldwide chip supply and, thereby, the worldwide economy.

It is for these reasons, and more, that we remain a “1” on the CAZ Scale, and we strongly believe that the risk/reward in traditional risk assets is not favorable. We continue to believe that the current opportunities in the private markets are significantly better than what is offered in public investments. There are always exceptions, and we do continue to find interesting special situations in listed securities. But our emphasis remains in the private markets, as we believe we are entering one of the most interesting environments that we have seen in quite some time.

Before this letter comes to a conclusion, it is critically important for readers to understand that we are not negative on everything, but we are very cautious. As we have always stated, our rating on the scale is not designed to be a market timing tool. It is meant to assess the overall risk/reward investors face and to inform their weightings within the allowable limits of their investment policy statements. This is not a time to throw caution to the wind, and it is a time to have protection in place for your portfolio. Most importantly, it is critical that investors tilt their portfolio to the investments that should provide the highest probability adjusted outcomes. That is what we are doing with our personal capital, and we strongly encourage you to do the same.

There are some important housekeeping items to cover. As you likely know, our firm has grown immensely, and we are honored to work with so many people from all around the world. With growth comes the requirement for new technology and new Team members to be able to scale. As part of our continued investment in people and processes, we are implementing a few new operational initiatives that should streamline communication for you, which will be announced over the next several quarters. The first initiative is now live and it entails the bifurcation of our “MyTeam” to distinct service responsibilities. Going forward, please use moneymovement@cazinvestments.com for everything involving money movements. This would include wires, capital calls, distributions, and transfers. Please continue to use myteam@cazinvestments.com for all other operational items. We are confident that this will help us serve you better.

Finally, First Freedom Art Company, a CAZ Investments company, launched a new online portrait gallery, featuring selected works from its Arnold Friberg Collection. We invite you to visit www.firstfreedomart.com, where you will find comprehensive videos and photographs of Friberg’s art in a gallery setting, as well as detailed information about:

- The life and legacy of Arnold Friberg

- First Freedom Art Company and its management team, and

- Friberg’s artistry, inspiration, and behind-the-scenes facts for Friberg’s paintings.

On the Gallery page, you can hear an audio clip of Arnold Friberg himself, describing the history behind his American masterpiece, The Prayer at Valley Forge.

Please tell your friends and family about First Freedom Art and follow them on social media.

We appreciate your partnership and look forward to connecting with you in the near future. All our very best!

The CAZ Investments Team