Quarterly Letters & Insights

CAZ Investments Quarterly Letter 2024 – Quarter 2

When Bad is Good and Good is Bad, but sometimes Bad is Bad and Good is Good

If that sounds like it does not make sense, welcome to the summer of 2024, where most investors in the world really want to see interest rates come down, but not if it means that we experience a recession. Thus, solid economic news is welcomed as news that we will not have a recession but then that exact same news is booed because it means the U.S. Federal Reserve (“Fed”) still has handcuffs on and cannot lower interest rates. Then, we get weak economic news which is celebrated because it means that the Fed will likely cut interest rates, only to have that same news send shockwaves through the markets because we may be in a recession…

Yes, that is precisely where we find ourselves in the summer of 2024. And, of course, we are not just dealing with interest rates. The escalation of hostilities between Israel and Iran, the new phase of the war in Ukraine, and the drama surrounding the U.S. presidential race has created a material number of new things for investors to digest. The volatility experienced these last few months has surprised most people, and it is unlikely that things are going to “settle down” between now and the end of the year.

The major factors we have covered in our recent letters remain very much in play, and we would strongly encourage you to go back and reread our 1st quarter letter that covers the 6 C’s that we believe summarize the state of the economy and markets in a concise manner. You can access that letter via our website by clicking HERE. The real title that we wanted to use for this letter was “Be Careful What You Wish For, Part 2.” That title is a “tip of the hat” to our 4th quarter 2023 letter that outlines precisely why the Fed is in a box, and why the expectations for interest rate cuts were completely misguided. We saw those expectations shattered as people realized the Fed simply did not have enough evidence to support rate cuts and they were determined to not repeat the mistakes of the early 80s. Please reread that letter, by clicking HERE, where you can see the evidence we used to support our position and how surprisingly similar it is to where we are now.

Most investors in the world right now are hoping for a goldilocks scenario where the economy can soften just enough for inflation to decline to acceptable levels but not so much to put us in a recession. The hope is that the inflation decline will enable the Fed to cut short-term interest rates enough to bolster the economy and avoid recession but not reignite inflation. As we have said many times, “hope is not a good investment strategy,” yet once again many investors are allocating capital based on an idealistic and unlikely result. History shows us that the goldilocks scenario rarely happens, and that significant pain is usually experienced by those who positioned themselves for the best case.

This pollyannaish behavior was on full display in June, when it seemed that the risks of the world just did not matter. It appeared that the market was going to grow to the sky with all eyes on the Magnificent 7, leading to their collective weighting of the S&P 500 growing to an eye-popping 33%! As a matter of fact, at one point, Nvidia by itself was worth more than the entire stock markets of Germany, France, and the U.K., combined! No one will argue that Nvidia is a fantastic company that is executing on all cylinders, but valuations still matter…

As we turned the page to the 2nd half of the year, along came a few data points that showed that perhaps the economy was softening much faster than people appreciated. Markets experienced an incredibly sharp decline, with the Nasdaq falling by more than 18% in a month, and many of the leaders like Nvidia plummeting by more than 35%.

This drop shocked investors, but they have proven to be undeterred and much of that decline in the mega-tech stocks, and therefore the major indices, has been erased by a rally that one could argue is being fueled by a term we have not used in many years, “The Fed Put.” There is a growing consensus that the Fed will cut aggressively at the September meeting and that will start the next easing cycle. Some forecasters were calling for an emergency cut in August and/or have predicted a “super cut” of 50 basis points at the next meeting. It is quite possible that the Fed will deliver a cut in September, IF the data we receive between now and then supports it, but we would be shocked if they did more than 25 basis points. Our view is that the Fed still realizes they are in a box and that the inflation dragon must be definitively slain before they can begin to feed the animal spirits once again.

The Real Economy is Struggling

There continues to be significant evidence that the “real economy” is facing material headwinds that must be considered as we look at the investment landscape. A few statistics can support that statement:

- Credit card and auto-loan defaults continue to escalate to levels that have not been seen since the Global Financial Crisis.

- Non-mortgage interest payments by U.S. households have nearly tripled in the last two years and are more than double the highest level ever recorded. (And, of course, mortgage interest rates are up a lot…)

- Job openings in the U.S. have declined dramatically, in all industries, with the exception of government jobs…

- More than half of new jobs created recently have been government jobs.

- Since 2019, native-born workers in the U.S. have collectively lost 1.5 million jobs.

- The non-farm payroll numbers reported have been consistently overstated and then adjusted down. The released numbers have been lowered by ~778,000 cumulatively since February 2022.

- Office building vacancy rates have now reached the highest level in history, at ~20%.

- Less than 25% of the stocks in the S&P 500 have outperformed the index itself, which is the lowest percentage experienced since at least 1980.

- Approximately 40% of the companies that make up the Russell 2000 index (Small Company Index) have NEGATIVE earnings.

- The very well-known Sahm Rule, which is triggered when the three-month average of national unemployment rises by 0.50% or more from its low over the last 12 months, is now saying we are in a recession.

There appears to be a widely held belief that interest rates coming down will heal all wounds and these issues will go away in short order. Make no mistake, rates coming down is definitely helpful but not every problem is a debt service or valuation metric problem. Some problems are just… problems. Supply and demand still matter, small business creation still matters, the regulatory environment still matters, and consumer demand still matters. All these factors have a major impact on the creation of jobs and wage growth, which are the overwhelming drivers of our economy.

One area on which we remain very focused is the commercial real estate market, as it has a massive impact on the health of the banks who have loan exposure to those assets, which then impacts dramatically the availability of capital to local communities, which then ripples through to small business creation/job creation/wage growth, which is ultimately the fuel the economy needs for sustainable expansion.

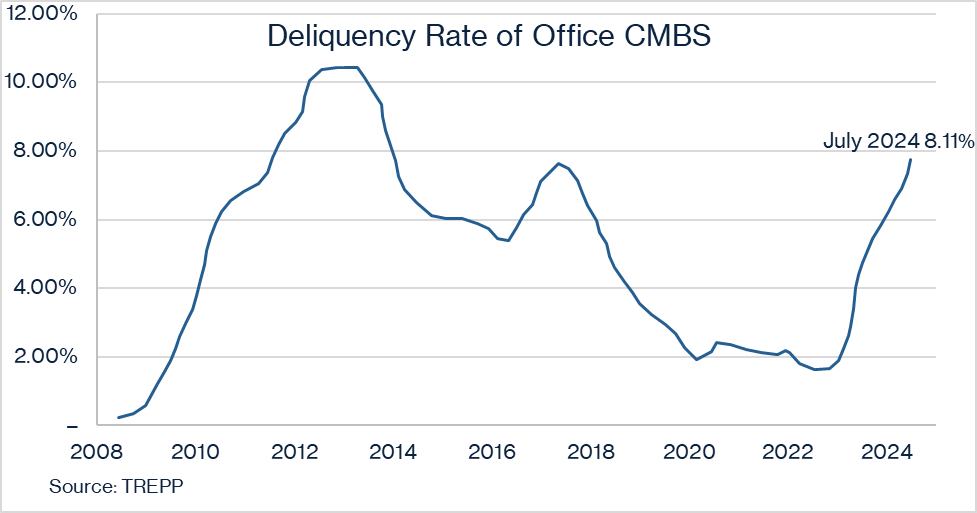

We have shown dozens of charts over the last several quarters to illustrate the potential pain that may be headed toward this segment of the real estate market, but this quarter we believe that one picture will indeed be equal to a thousand words:

What this chart shows clearly is that delinquency rates on commercial real estate loans are rising at an alarming rate, more than quadrupling in less than 2 years. We have not seen this dramatic acceleration in problem loans since the Global Financial Crisis. The only conclusion that one can reach when looking at this data is that bankruptcies are likely to increase significantly from current levels.

Everyone keeps waiting for the shoe to drop in this sector and this chart provides strong confirmation that we are entering a new cycle of pain. There is evidence that this is already happening. One example would be that, as of June 2024, California recorded 214 commercial foreclosure filings, marking a 289% increase compared to the same period last year. (As a side note, as discussed above, this problem ripples straight through to the banks. In California, 31% of all banks have commercial real estate loans outstanding that total at least 3 TIMES their capital base…)

Opportunities Among the Uncertainty

Sometimes opportunity comes from uncertainty and sometimes it comes despite uncertainty. Right now, we believe there is a little bit of both. One can ascertain from the commentary above that we are concerned about many things. That is true, but we also see some very interesting paths to solid risk adjusted returns. Thus, we do not believe that a one size fits all strategy is the smart decision at this time in the cycle.

It is for the reasons above, and more, that we remain a “1” on the CAZ Scale, and we strongly believe that the risk/reward in traditional risk assets is not very favorable. There are dislocations in the public markets that are interesting, and some solid values to be found, but we just continue to see incredibly attractive opportunities in less-correlated assets. We have been quoted saying that we are seeing some of the best values in the private markets that we have seen in decades.

Everyone who knows us is aware that we are very thematic investors, and our core themes continue to provide us with excellent risk adjusted returns, such as Growth of Private Assets, Energy Evolution, Changes in Consumer Behavior (Professional Sports), Disruptive Technology, and Secondary Opportunities. We are also seeing some new themes developing that we are actively pursuing, such as The Changing Needs for Military Readiness.

The lack of capital, and/or new developments, in several of these areas is presenting us with some outstanding risk/reward opportunities. We look forward to sharing more details with you as they are fully diligenced and we decide they are worthy of our personal capital.

It is hard to believe that we are already in the back half of the year, and we look forward to a very exciting few months as we close out 2024. As a reminder, our annual Themes event will be held live in Houston on January 16th, 2025, with activities planned for the afternoon and evening of January 15th as well. Please hold that date on your calendar and start booking your travel as needed. We appreciate your partnership and look forward to seeing you very soon!

The CAZ Investments Team